By: David M. Williams

December 9, 2010

Was there a clear signal when the British Empire was eclipsed by its colonies? When the New Economy pushed aside the old?

In the digital world, we may have just witnessed such an event.

Wednesday saw two of China’s most visible Internet players go public on US exchanges. Despite raising the filing ranges on both, and pricing each above those ranges, both shot up to levels that provide a clear signal that Chinese Internet companies are increasingly in the pole position. It has been a decade in the making, but investors are now not only willing to concede that China’s players are worth more (per dollar of revenues or earnings) than their Silicon Valley counterparts, they’re willing to bet on Chinese businesses without first having seen the movie play out before in the US. The message: growth rules.

Investors will pay more for the Amazon.com of China (Dangdang) than for Amazon itself. The YouTube of China (Youku) is welcome to tap the US markets even before its Silicon Valley counterpart. Investor demand drove shares of both companies far higher in the aftermarket, with Dangdang (DANG:NYSE) rising 86.9% to close at $29.91 and Youku (YOKU:NYSE) climbing 161% to close at $33.44. Youku set the record for the biggest one day gain since Baidu’s blockbuster IPO in 2005.

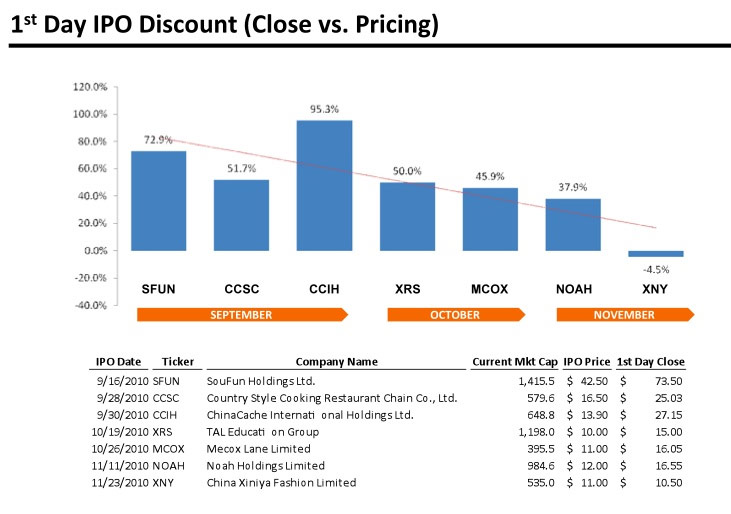

While not the first Internet IPOs out of Asia to go public this cycle and immediately trade up, these two stand out. At the very beginning of each upturn, Asian Internet IPOs are priced in line with – or lower than — their US counterparts. However, investors pay up for growth and immediately bid those shares up in the aftermarket to reflect it. As it becomes clear what type of premiums investors are willing to pay for varying levels of growth, underwriters usually narrow the gap over time by pricing the next IPOs at higher multiples. That usually implies a decline in first day pops (before allowing for individual company differences).

Wednesday’s debuts, however, were anything but typical. Their performances reflect unique attributes. Dangdang, China’s No. 1 bookseller online, is, like Amazon.com, more than just a bookseller. The Dangdang.com flagship site is well established across the consumer market. Backed by top venture firms in Silicon Valley and China such as DCM, it has been a long-anticipated listing, as its competitive position is solid, it has a meaningful operating history with significant revenues and it has turned a profit. Most importantly, it is seeing top-line growth north of 50% off of that base. For investors, Dangdang represents a chance to invest in a known business model, a proven team, and participate early in a rapidly growing, and, ultimately, a very large market.

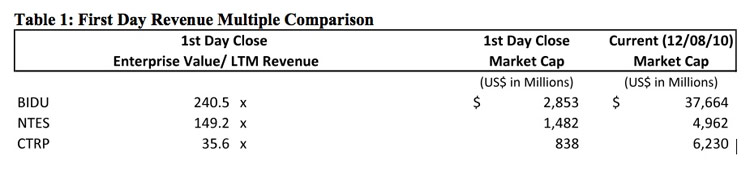

At the first day close, DANG is valued at $2.3 billion, which represents 7.7x latest 12-month revenues (vs. ~2x for AMZN). However, the rapid growth makes a 12-month comparison stale. The spread narrows when looking at the third quarters annualized, and presumably converges if growth continues at a reasonable pace into the near future. Youku is also No. 1 in its market – online video — and has an experienced management team led by founder Victor Koo (previously COO of SOHU). It has blue chip backers including firms such as Sequoia. From there the comparison with Dangdang diverges. A younger company in a younger sector, Youku’s ad-based business model yields a smaller base of revenue ($17.2 million in Q3), but is growing at an even faster pace (over 100% year-over-year). The company is not yet profitable. At its first day close, it has a market capitalization of $3.3 billion, implying a multiple of around 100x latest 12-month revenues.

Even annualizing its latest quarterly revenue of $17.2 million still implies a revenue multiple of around 50x. Even so, other China net listings have gone on from high initial double – or even triple – digit revenue multiples to yield strong returns over time (NTES, BIDU, CTRP etc.). With that higher multiple comes an expectation to deliver exceptional rates of growth.

Although somewhat of a hybrid model with elements of YouTube, Hulu and possibly Netflix, Youku is regarded as the “YouTube of China”. Without a close public US comparable off of which to value the company, the offering is unprecedented. Instead of representing a source of negative uncertainty, Youku actually benefitted as the first major vehicle to satisfy worldwide investor interest in the Internet video space, and has now set the bar against which US players may be measured.

Over the last few years, leading US Internet players have tended to wait as long as possible to go public. However, as lines between national markets continue to blur over time, the Facebooks and YouTubes of the world may conclude that allowing others the advantage of tapping the US equity markets — the most affordable capital available – while limiting themselves to the private markets, is an unacceptable risk to take for any meaningful period of time.

China’s digital elite have demonstrated time and again how difficult it is for foreign firms to compete in a very local market. While both Dangdang and Youku are focused on the Chinese market near-term, now that they have access to US capital at inexpensive levels, perhaps the relevant question going forward is how difficult will it be for Chinese companies to play in the US market?

By: David M. Williams

March 24, 2011

While we’ve seen a pickup in initial public offerings of late, most notably in Q4 2010 prior to the holiday slowdown, many people watching the market continue to expect muted IPO market prospects relative to the 1990s. Maybe that’s not such a bad thing. The last time there was anything approaching a positive consensus was early 2000, and we know how that ended.

Sarbanes Oxley? Frivolous lawsuits? There are many reasons to stay private if it’s a close decision. However, it is no longer a close call. Investor demand for growth and the resultant multiples now available are so compelling that companies young and old (by IPO standards) can no longer afford the luxury of remaining private.

See No IPOs

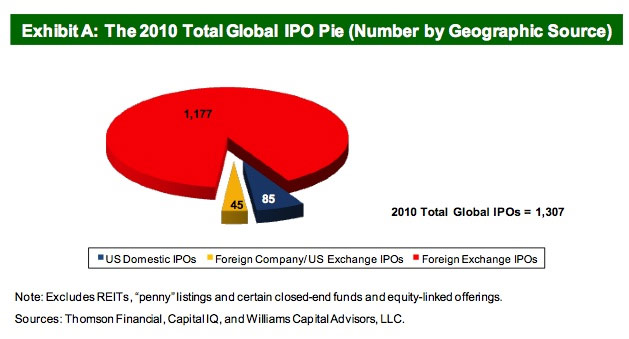

The IPO markets overall are highly receptive. We just don’t see it locally – as reports of IPO volume commonly exclude not only listings on overseas exchanges but also listings of foreign companies (many of them backed by US VCs) here in the US via American Depositary Receipts (ADRs). Listings by non-US companies didn’t rally much attention back when Silicon Valley’s Sand Hill Road was the undisputed champion of the IPO-generation machine, but they’re a major factor now that the market’s digital and clean-tech debutantes increasingly hark from Beijing or Bangalore rather than Palo Alto. In 2010, US companies accounted for only 85 listings at home, while 45 overseas companies made their public debuts on NYSE, AMEX or NASDAQ. The majority of IPOs, 1,177 for the year, represented international companies listing on non-US bourses.

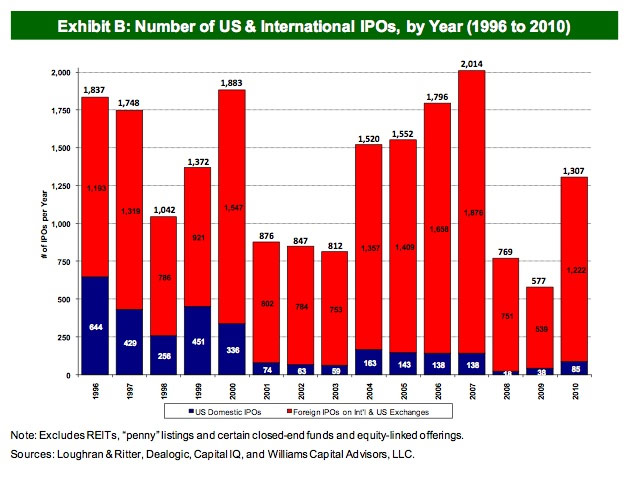

This phenomenon is not unique to 2010 (Exhibit B). In fact, the 2000 worldwide record of 1,883 new listings was already toppled in 2007, with 2,014 IPOs globally, netting $298.8 billion. While 2010’s world total of 1,307 IPOs and $280.1 billion in proceeds is not a new peak, it is multiples of the 85 or so domestic IPOs we see reported here in Silicon Valley.

Looking only at US IPOs, the last decade has seen a drought of biblical proportions. That said, there are two good reasons to believe that the uptick in IPOs at the end of 2010 (US and international) will gain even more steam during 2011: increasing Supply and even stronger demand.

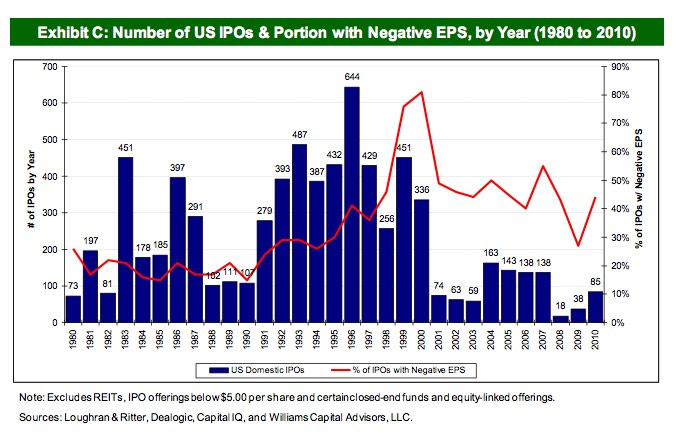

Supply: Previous droughts of even a few years were generally followed by floods of activity (Exhibit C). Moreover, a look back to 1980 reveals that 1999/2000 was not even a one-time peak of US IPO activity – it simply represented the end of a multi-year boom, where the numbers of listings each year wasn’t as notable as the nature of companies being listed. The fact that over 80% of listings were unprofitable, and those companies garnered more attention than those in the black, was the hallmark of the Internet Bubble. Profitable and not, the “supply” of list-able companies – after a decade long drought – is significantly greater today than was the case in 99/00 after eight strong years of IPOs had depleted the supply of even the most marginally list-able candidates. The US listings to date this cycle have barely made a dent, and the best (i.e. IPOs of the leaders) is yet to come.

Taking a company public prior to break-even is not uncommon; going public years prior to projected profitability, with additional follow-on financings required keeping the company afloat … that was unsustainable.

Demand: Equity investors are clamoring for growth, as the scramble to obtain shares in Facebook illustrates. In a record low interest rate environment, there is an unfulfilled demand for growth companies to absorb increasing inflows of capital allocated for such investments. If the landscape leading into 1999 and 2000 was particularly fertile for the IPO market, the catalysts for 2011 are far stronger.

Beyond macroeconomic factors, the phenomenal growth, profit margins and network effects promised by some IPOs of the late 90s are not only on the table once again, but the drivers are arguably stronger this time around. A company like Facebook represents a stronger example of financial and competitive accomplishment than even Netscape back in 1995.

Hear No IPOs

The press is littered with the unfulfilled predictions by management teams of an IPO in the near future. Whether it is wishful thinking, bad luck with market conditions or operational stumbles, such pronouncements rarely play out.

On the flip side, the companies who say they won’t go public in the near-term, or better yet, don’t say anything at all, make up the bulk of the successful listings year in and year out.

The reason we should assume the dam will break, and companies (both over-ripe and still green) will list? The valuations are becoming so compelling that remaining private will simply not be a viable option – particularly if a direct competitor taps the capital markets in the interim.

A Question of When, not If

The SEC interest in feeder funds is just one sign that these companies “should” go public and enjoy the benefits of a listing, as they’re already facing many of the related headaches and costs.

If the year 2001 was the year where we looked back and realized we had already listed anything that “could” be listed, the current supply of list-able companies presents an inverse portrait. 2011 should be the year the dam breaks – for all of the companies that “should” have listed (absent the alternative markets which have popped up to provide capital). Over the past decade, we’ve not only replenished the pool of start-ups, but some of them have been able to ripen well past the point of traditional IPO harvest, nourished by these alternative capital pools.

Foregoing a public listing means a higher cost of capital. Certainly the valuations attached to recent investments in web companies (both direct and via exchanges such as SharesPost and SecondMarket) seem attractive – and they are. But the valuations afforded by the public market are higher – or else these investors wouldn’t be making such bets. The December IPO of Chinese online video leader Youku provides a hint of the possible valuations achievable for digital leaders in the public markets. Youku’s valuation is not indicative for most IPO candidates. That said, at least for the time being, it appears to be trading at a trailing revenue multiple a few times as high as Facebook is changing hands privately of late. In both cases, those trailing revenue multiples are irrelevant; forward estimates of earnings (accurate or otherwise) are driving valuations – but it is the public/private differential that stands out.

To take it a step further, there’s an argument to be made that these firms “must” go public in 2011 (if not a few quarters later). A decision to remain private is not made in a competitive vacuum. Failing to tap the cheapest pool of capital can be a fatal decision if a competitor does and the IPO window closes behind them.

Among the arguments to expect a continued paucity of Silicon Valley IPOs is that there just aren’t enough candidates from a bottoms-up perspective. The argument is valid if you make a few key assumptions about who could or should go public. Larger investment banks generally counsel companies to wait until they have ~$100 million in revenues to go public. By that metric, there isn’t a wave of IPOs on the horizon. However, if past is prologue, that doesn’t account for two factors that occur every major IPO cycle, and at an accelerated pace each successive boom:

Size Matters?

With the shrinking number of investment banking firms over the last decade, perceptions of the IPO market are colored by the lens of the few large investment banks left standing. It is true that underwriters prefer to take companies public when the deal size (revenues aside) is at least $100 million.

However, back when the IPO market in the US was far more robust, $50-75 million dollar IPOs were common. This perception that IPOs “should” be at least $100 million to matter has affected the way even third parties measure the market, as many reports on the state of the IPO market exclude listings below $100 million.

IPOs of less than $100 million rose above the 50% level in 99/00, but that wasn’t the first time. In fact, even after accounting for inflation, the key difference between this past decade and previous decades is the extraordinary absence of these listings – the bread and butter of the IPO market up until recently.

To butcher an already ignominious expression, it’s not the size of the (revenues) boat, but the motion of the (earnings) ocean that matters. Basically, in a low rate environment, a tally of last year’s receipts matters little relative to the earnings expected this year and next, as well as the rate of increase beyond.

650-714-0625

Chelsey@WilliamsCap.com

610 Kingsley Ave.

Palo Alto, CA 94301

Powered by Ventnor Web Agency

Copyright © Williams Capital Advisors 2023. All rights reserved.