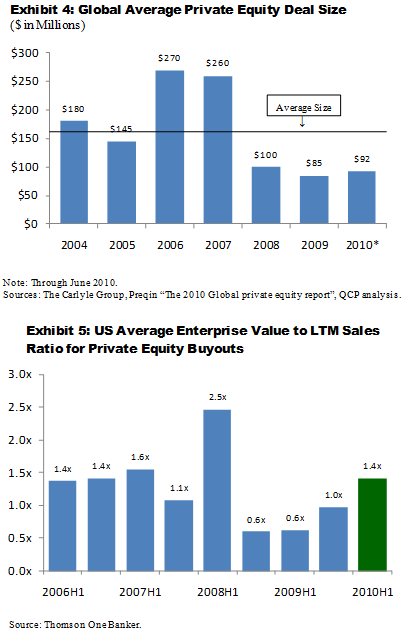

The average buyout remains below the $100 million mark (Exhibit 4). While that may have been a reflection of distressed sellers and compressed valuations in late 2008 through 2009, valuations in 2010 have rebounded well beyond levels normally seen early in a cycle (Exhibit 5).

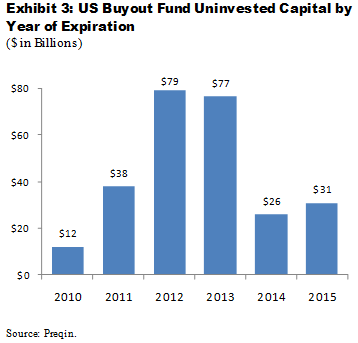

Some private equity firms are seeking extensions to provide for more time to invest funds with approaching anniversaries (see “Limited Partners Fear Coming ‘Distressed Buying’ Boom,” WSJ…). Some such extensions may be granted, but the overall volume of investable dollars tied to expiration dates is so large that effects will continue to be felt in the marketplace for some time.

Even as individual funds approach their 5–year anniversaries, we’re unlikely to see eye-popping valuations driven by a use-it-or-lose-it mentality. Instead, we’re likely to see a continued shift towards a sellers’ market as competition for a limited number of financeable companies continues to heat up.

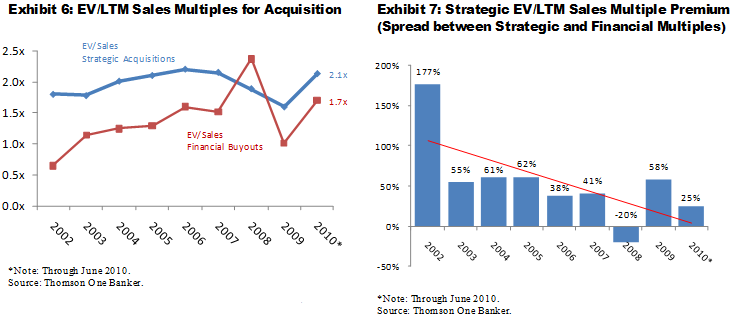

For middle & lower-middle market companies, the most visible impact is already apparent in valuation multiples. Not only are valuations rising rapidly on an absolute basis, the historic gap between prices and paid by strategic acquirers relative to financial buyers is narrowing and financial buyers are increasingly the winning bidders for Silicon Valley companies (Exhibit 6 and 7).